%20(750%20x%20500%20px).png)

If you have been following tax developments, you have probably heard about Qualified Small Business Stock (QSBS). Under Section 1202 of the Internal Revenue Code, a shareholder who holds QSBS for the required period can exclude up to 100% of their capital gain from federal income tax when they sell. For stock issued after July 4, 2025, the One Big Beautiful Bill Act (OBBBA) shortened the required holding period and expanded the benefit.

That is a compelling headline. But for many Pennsylvania small business owners, the real question is more nuanced: Does the annual tax cost of operating as a C corporation outweigh the capital gains savings you would receive at sale?

As I have discussed in previous posts on deal structure and tax considerations when buying or selling a small business, entity selection and deal structure can significantly affect what you take home. This article walks through the QSBS tradeoff, including hypothetical analysis scenarios, to help you and your tax advisor evaluate whether C corporation status might make sense for your situation.

What Changed Under the OBBBA

The OBBBA, signed into law on July 4, 2025, made several important changes to Section 1202. For stock issued after that date:

- Tiered exclusion: 50% exclusion after 3 years, 75% after 4 years, 100% after 5 years

- Higher gain cap: Up from $10 million to $15 million (or 10x the taxpayer’s adjusted basis, whichever is greater)

- Higher asset threshold: The issuing corporation can now have up to $75 million in aggregate gross assets, up from $50 million

- Inflation indexing: Both the $15 million cap and $75 million threshold will adjust for inflation beginning in 2027

Stock issued before July 5, 2025, remains subject to the prior rules: a full five-year hold for any exclusion, and the $10 million gain cap.

The Core Tradeoff

QSBS is only available to owners of domestic entities taxed as a C corporation. S corporations, LLCs taxed as partnerships, and sole proprietorships do not qualify under Section 1202.

So the question becomes: What does C corporation status cost you each year, and does the QSBS exclusion at sale more than make up for it?

Federal Tax Comparison: C Corp vs. S Corp

C Corporation: Double Taxation in Action

A C corporation pays a flat 21% federal income tax on net income. When the corporation distributes after-tax profits to shareholders as dividends, the shareholder pays tax again, at the individual level, typically at the qualified dividend rate of 15% or 20%, plus the 3.8% Net Investment Income Tax (NIIT) for higher earners.

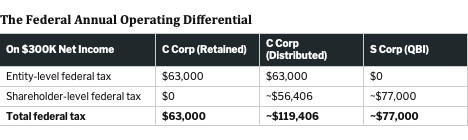

In a hypothetical scenario: on $300,000 of net income, fully distributed to a single high-income shareholder:

- Corporate tax: $300,000 x 21% = $63,000

- After-tax available for distribution: $237,000

- Shareholder dividend tax (at 23.8%): $237,000 x 23.8% = $56,406

- Total federal tax: $119,406

- Combined effective rate on distributed income: ~39.8%

Many C corp owners retain earnings rather than distributing them, which defers the second layer of tax. This creates a “lock-in” effect: the money stays in the business, taxed once at 21%, and any additional tax is deferred until a distribution or sale. If the owner is reinvesting all profits, the C corp can be tax-efficient during operations. But if the cash is ever distributed out of the entity, the deferred tax eventually comes due. There are strategies in some instances in conjunction with the sale of the business where the treatment of retained cash can be negotiated as part of the sale to recognize tax efficiencies.

S Corporation: Pass-Through with QBI Deduction

An S corporation passes income through to the shareholder, who pays individual income tax on the full amount. The Section 199A QBI deduction, now made permanent by the OBBBA, allows eligible owners to deduct up to 20% of qualified business income from taxable income.

In the same hypothetical: on $300,000 of net income (after reasonable salary of $120,000):

- QBI deduction (20% of $180,000 pass-through income): $36,000

- Effective taxable pass-through income: $264,000

- Federal tax at blended effective rate: approximately $73,000 to $82,000

- No second layer of tax on distributions

For a married filing jointly owner in the upper brackets, the effective federal rate on S corp business income after the QBI deduction is approximately 29.6%, compared to 39.8% on fully distributed C corp income.

In the hypothetical, if all earnings are retained, the C corp costs about $14,000 less annually in federal taxes than the S corp. But the moment you distribute, the C corp costs roughly $42,000 more. This is the double-taxation reality.

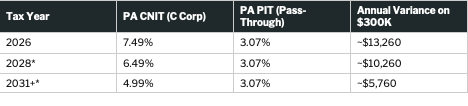

Pennsylvania Makes It Worse for C Corps

Pennsylvania imposes a Corporate Net Income Tax (CNIT) on C corporations at rates that are significantly higher than the state’s flat personal income tax:

*This assumes statutory rate reductions occur as scheduled. If rates were to increase or pause, the analysis changes.

Over an 8-year hold beginning in 2026, the cumulative PA state tax differential on $300,000 of annual net income is approximately $75,000 to $85,000 in additional state tax paid as a C corp compared to an S corp.

Pennsylvania Does Not Conform to QSBS

This is the other critical piece: Pennsylvania is one of only four states that entirely decouple from Section 1202. Even if you qualify for a full 100% federal QSBS exclusion, Pennsylvania will tax the entire gain at 3.07%, just like any other capital gain. The QSBS benefit for a Pennsylvania resident is exclusively a federal benefit.

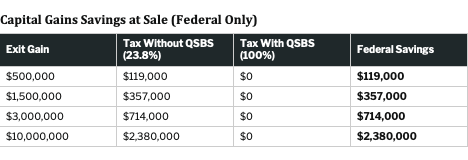

The Breakeven: When Does QSBS Pay Off?

Using our hypothetical $300,000 in annual net income and an 8-year holding period, here is how the numbers look at different exit values. We assume the owner is a high-income, married filing jointly PA resident, the C corp retains most earnings, the federal LTCG + NIIT rate is 23.8%, and the S corp uses the 199A QBI deduction at 20%.

Even assuming the C corp retains earnings and captures the federal deferral advantage, the net annual operating cost of C corp status (PA CNIT differential minus federal retention benefit) works out to roughly $0 to negative $3,000/year. For a disciplined owner who does not distribute, the annual operating cost differential is relatively modest.

But if the C corp distributes even some of its earnings, the math shifts dramatically. An annual distribution of $150,000 in dividends adds approximately $35,000/year in combined additional tax over the S corp.

PA taxes the gain at 3.07% in all scenarios, regardless of QSBS status.

The Bottom Line

For owners who retain earnings and plan to sell after 5+ years at a gain of $1 million or more, the QSBS federal savings will often exceed the cumulative operating tax cost of C corp status. The benefit can be better at higher exit values.

The math gets closer when:

- The business distributes earnings regularly (double taxation erodes the annual advantage)

- The exit gain is below $500,000

- The holding period is long (10+ years) and distributions are made, compounding the annual differential

- The business does not ultimately qualify for QSBS at sale

When QSBS May Not Work

Several factors could undermine the strategy:

- Excluded businesses: Section 1202(e)(3) disqualifies service businesses in health, law, engineering, accounting, consulting, financial services, and several other categories

- Holding period not met: No exclusion is available if you sell before 3 years (post-OBBBA stock) or 5 years (pre-OBBBA stock)

- Gross assets exceed the threshold: The $75 million cap must be met at the time stock is issued

- Not acquired at original issue: QSBS must be acquired directly from the corporation, not purchased from another shareholder.

- S Corporation stock. Existing S corporations that revoke their election and become C corporations cannot retroactively qualify their outstanding stock as QSBS - only newly issued stock, for new consideration, after the entity is taxed as a C corporation will qualify, and only post-conversion appreciation is eligible for the exclusion.

- Gain exceeds the cap: While $15 million is generous, larger exits may only partially benefit

A Note for Business Acquirers

If you are acquiring an existing business, the QSBS analysis requires additional planning. Because QSBS must be acquired at “original issue,” buying stock from an existing shareholder does not qualify. Instead, the acquirer typically forms a new C corporation, contributes capital in exchange for stock, and uses the new entity to acquire the target’s assets. The holding period begins when the new stock is issued, not when the target business was founded.

Final Thought

The OBBBA made QSBS more powerful and more accessible. For the right business, in the right circumstances, the federal savings at exit can be transformative. But C corporation status is not free. The annual operating cost, particularly in Pennsylvania where the CNIT is high and the state does not recognize the QSBS exclusion, is a real consideration.

QSBS is not a planning gimmick. It is a structural decision with long-term consequences. The right choice depends on whether your likely exit path supports it. This is a conversation that should involve your attorney, your CPA, and ideally your financial advisor, and it should happen early, before the entity is formed or the deal is signed.

If you are starting a business, acquiring one, or considering a conversion, I would be happy to walk through how entity structure and deal planning could affect your outcome. Reach out, and let’s find a time to talk.

This content is for general informational purposes only and is not legal or tax advice.